Agents hate this guide. Because this guide tells you the truth they can’t afford to tell you.

At a glance

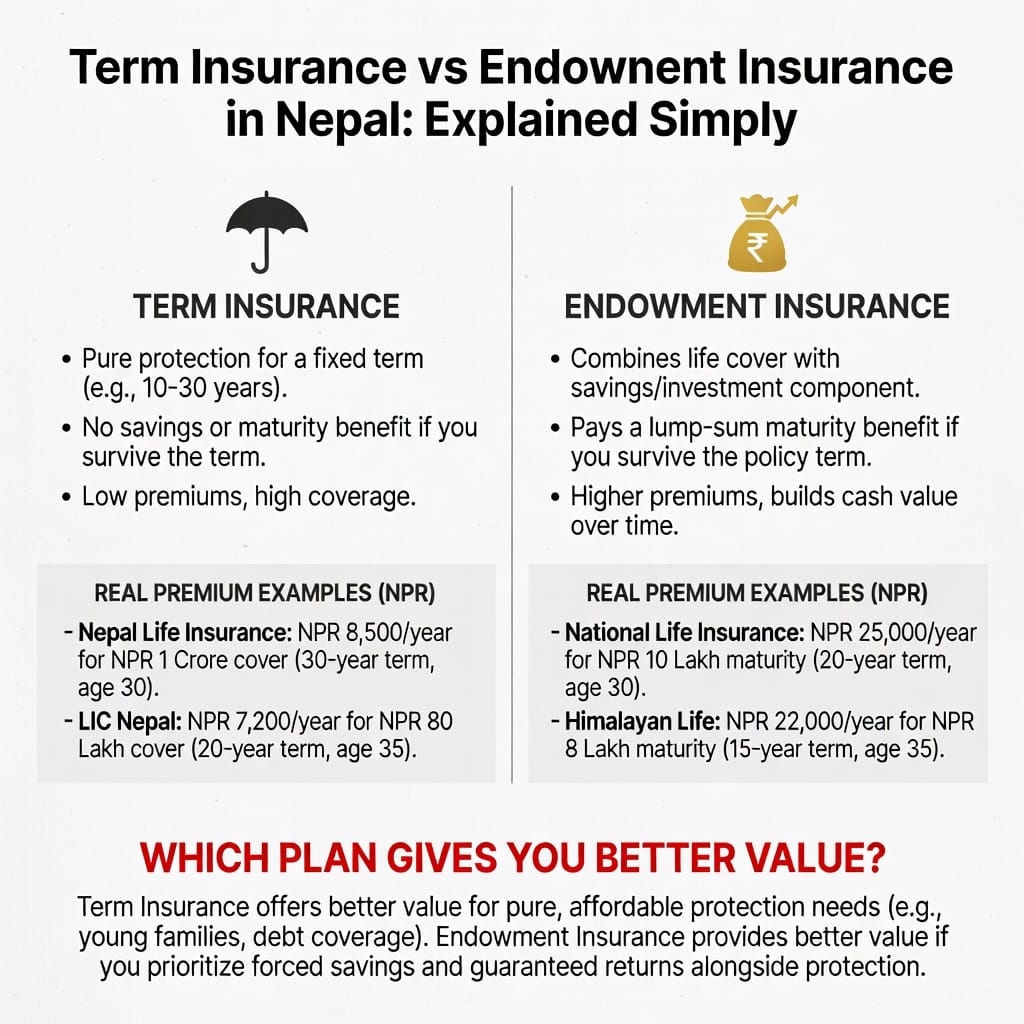

Where your premium goes — and what comes back

Term

protection only

Annual premium

Every rupee buys protection — no savings portion.

What comes back

- Die during the term — your family receives the full sum assured, tax-free.

- Outlive the term — nothing comes back. The premium was the cost of cover.

Endowment

protection + savings

Annual premium

What comes back

- Die during the term — your family receives the sum assured.

- Reach maturity — you receive the sum assured plus accumulated bonus, guaranteed.

Same person, same sum assured: term costs far less but pays only on death; endowment costs more and always pays — the extra premium is your savings, not better cover.

Endowment insurance pays an agent far more commission than term insurance does, in rupees. It is not just a higher rate (the regulated first-year cap is 25 percent for endowment against 10 percent for term life); that higher rate is also applied to a much larger premium, because endowment costs many times more than term for the same sum assured. So an agent can earn many times more, in rupees, by selling you endowment rather than term. That is why almost every agent you meet will push you toward an endowment plan — and call it the “smart” choice. It is smart. For them.

This guide gives you the unbiased comparison, the correct numbers, and a simple rule to decide which product is right for your situation.

One Sentence Each

Term insurance: You pay a small premium for pure life cover. If you die during the term, your family gets the full payout. If you survive, the policy ends and you receive nothing back — and that is exactly why it is affordable.

Endowment insurance: You pay a larger premium for life cover plus a savings component. If you die, your family gets the sum assured. If you survive to the end of the term, you receive the sum assured plus all accumulated bonus. You always get something — which is why it costs much more.

Term beema ra endowment beema ma ke farak cha?

Term insurance (jeevan suraksha beema) pays a death benefit only if you die during the policy period — there is no payout if you outlive the term. Endowment insurance (bachat beema) pays a lump sum on death

OR at maturity, because part of your premium is saved and returned to you with bonuses.

Nepal ma jeevan beema kina lini parcha?

Life insurance protects your family’s income if you die unexpectedly — covering daily expenses, children’s education, and outstanding debt. In Nepal, most bank loans and home loans now require a life

insurance policy as collateral. Both term and endowment plans fulfil this requirement under NIA regulations.

Beema ma nominee kasari rakhne?

Your nominee receives the death benefit if you pass away. Choose someone financially dependent on you — your spouse, children, or parents. You can nominate more than one person with a percentage split.

Always update your nominee after major life events such as marriage or the birth of a child.

Side-by-Side Comparison

| Feature | Term Insurance | Endowment Insurance |

|---|---|---|

| Purpose | Pure protection | Protection + savings |

| Annual premium (Rs. 25L, age 30, 20yr, model estimate)* | ~NPR 9,800/yr | ~NPR 122,000–127,000/yr |

| Death benefit | Full sum assured | Full sum assured + bonus accrued |

| Maturity benefit | Nothing | Sum assured + accumulated bonus |

| Loan facility | No | Yes (after 3 years) |

| Surrender value | No | Yes (after 3 years) |

| Tax deduction on premium | Yes | Yes |

| Annual bonus | No | Yes (declared by the insurer) |

| Best for | Maximum cover, tight budget | Forced savings, specific financial goal |

*Premiums are illustrative outputs of our calculator’s model for this profile, not quotes from NIA or any insurer. Run your own figures in the calculator.

The Real Cost — A Nepal Example

Sunita is 30 years old, working in Kathmandu, and wants Rs. 25 lakh of cover for 20 years from Nepal Life. Here is how the two plan types compare in our calculator’s model (real premiums vary by insurer):

| Term (Rakshya Kawach) | Endowment (Sunaulo Bhabisya) | |

|---|---|---|

| Annual premium (model estimate) | ~NPR 9,800 | ~NPR 125,000 |

| Total premiums over 20 years | ~NPR 1.96 lakh | ~NPR 25 lakh |

| Maturity payout | Nothing | Rs. 25 lakh + accumulated bonus |

| Death benefit (any time in term) | Rs. 25 lakh | Rs. 25 lakh + bonus accrued |

| Premium freed up by choosing term | ~NPR 1,15,000 per year | |

Premiums are illustrative outputs of our calculator’s model for this profile, not quotes. Sunaulo Bhabisya’s declared bonus for FY 2081/82 is Rs. 60 to 65 per Rs. 1,000 of sum assured per year, so the exact maturity value depends on the bonus the insurer declares each year. Verify current rates with Nepal Life.

The “Invest the Difference” Question

Choosing term frees up roughly NPR 1,15,000 a year. If Sunita invests that difference steadily over 20 years (in a fixed deposit or mutual fund, for example), it can grow into a corpus broadly comparable to the endowment’s maturity value, while she also keeps the full Rs. 25 lakh of life cover throughout and her money stays liquid.

The honest verdict is that the two come out close, and which one wins depends on three things: the bonus the insurer actually declares, the return you actually earn on the invested difference, and, most of all, whether you stay disciplined. If you will genuinely invest the difference, term plus investing tends to edge ahead and gives you far more flexibility. If the money would otherwise be spent, the endowment’s forced savings have real, tangible value.

What Term Cover Actually Costs Across the 14 Insurers

Here is the part agents rarely mention: for pure term cover, the 14 licensed insurers price very close to one another. The base term rate for a given age, sum assured, and term sits in a narrow band, so the same profile produces broadly similar premiums almost everywhere. For NPR 50 lakh of cover at age 28 on a 20-year term, the gap between the cheapest and the dearest insurer is usually only a few thousand rupees a year, on the order of a few hundred rupees a month.

Not sure which plan fits you? Answer 5 questions and get a personalised match.

Find My Plan →That means price is rarely the right thing to choose a term insurer on. What actually varies between companies is their claim settlement record, their financial strength, and the riders they offer. Decide how much cover you need first, then choose the insurer on those.

To see your own number, enter your age, sum assured, and term in our premium calculator, which ranks all 14 insurers cheapest first. To compare them on claim settlement, see our claim settlement ratios page.

When Term Insurance Is Clearly the Right Choice

1. You have a mortgage or large loan. Size your term policy to match your outstanding balance. If you die, your family keeps the house. Term is the cheapest way to achieve this — and the most logical.

2. You are young, have dependents, and have a tight budget. At age 28, you can get Rs. 25 lakh of cover for under Rs. 10,000/year — less than Rs. 900/month. Nothing else in Nepal’s financial market gives your family this much protection for this little money.

3. You are a foreign worker. If you are working in the Gulf, Malaysia, Japan, or elsewhere, all 14 Nepal life insurers cover death outside Nepal as standard. Maximum cover. Minimum cost. Simple claim process for your family at home.

4. You are a disciplined investor. If you will invest the premium difference — in FDs, mutual funds, or real estate — term plus investment beats endowment mathematically in most scenarios across most time horizons.

When Endowment Insurance Makes More Sense

1. You are not a disciplined saver. If your money disappears before the end of the month, the endowment’s forced savings are genuinely valuable. The policy commits you to saving — and rewards you with a lump sum at maturity.

2. You have a specific future goal. Children’s university fees in 18 years. A house deposit in 20 years. Endowment is designed for this — it turns a regular premium into a guaranteed lump sum at a date you choose.

3. You need to borrow against your policy. Endowment plans allow policy loans after 3 years of premiums. Term plans do not. If liquidity access is important, endowment is the only option.

The Simple Decision Rule

Answer these two questions:

- Will you invest the premium difference if you buy term? If yes → buy term. If no → consider endowment for its forced savings value.

- Do you have a specific lump-sum goal in 15–25 years? If yes → endowment is built for this. If no → term is almost certainly better value.

Use our Premium Calculator to see exact premiums for both plan types across all 14 insurers with your specific age and sum assured.

Data source: NIA Annual Report FY 2081/82. PremiumThe regular payment you make to keep your insurance policy active. Full definition → figures are illustrative model estimates, not quotes; verify with insurers before purchase. Past bonus rates do not guarantee future bonus declarations. Claim ratios are amount-based (NPR Crore per NIA Schedules 14 & 15); per-company claim settlement counts are not separately published — only an industry-wide total is available. See full disclaimer →