Your premium is the price tag of your life insurance, but very few buyers in Nepal can explain what actually sets that number, or what happens to it after they sign. Two people the same age can pay wildly different amounts for the “same” cover, and an endowment buyer can end up paying in almost as much as the policy is worth. This guide breaks down exactly what you are paying for, what moves the number up or down, and the rules that decide whether your policy stays alive.

If you are still weighing whether to buy at all, start with why life insurance in Nepal is non-negotiable. This guide assumes you have decided to buy and now want to understand the cost.

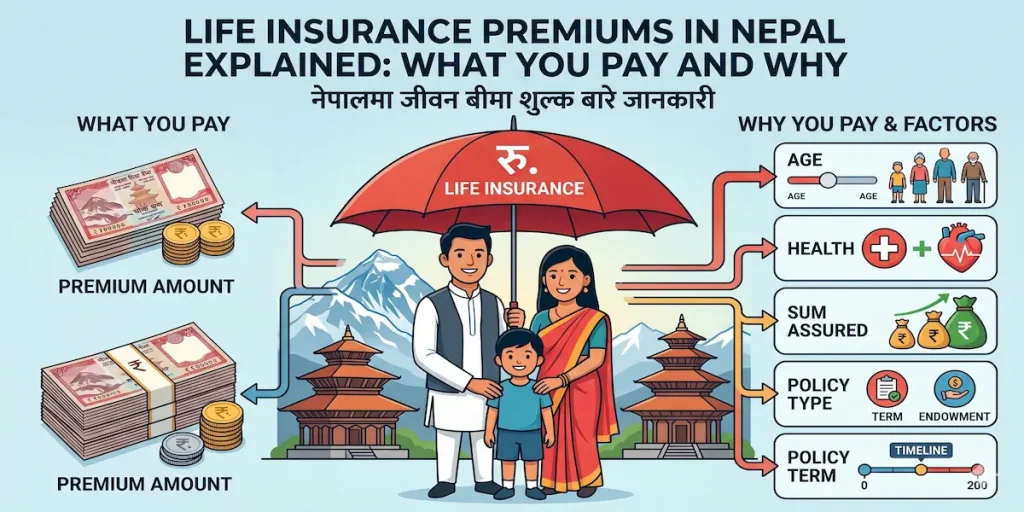

What a “premium” actually buys

A premium is the amount you pay an insurer (yearly, half-yearly, quarterly, or monthly) to keep your policy in force. In a term plan, almost the entire premium pays for pure life cover, which is why it is cheap. In an endowment or money-back plan, your premium is split: a slice pays for the life cover, and the larger part is set aside as savings that grow with bonuses and come back to you at maturity. That split is the single biggest reason savings-type premiums are many times larger than term premiums for the same sum assured.

What actually decides your premium

Four inputs do almost all the work. You can see them interact in real time in our premium calculator, but here is what each one does:

- Your age. Premiums rise with the age at which you buy. An insurer prices the risk of paying out, and that risk climbs every year you wait. Buying at 30 instead of 40 locks in a lower rate for the entire term. This is why “I’ll get it next year” is the most expensive sentence in insurance.

- Sum assured. The premium scales almost directly with cover. Double the sum assured and you roughly double the premium. Decide the cover you actually need first (our need-assessment tool sizes it), then price it.

- Policy term. Term length pushes premiums in opposite directions depending on plan type. For a term plan, a longer term spreads risk and the yearly premium tends to ease. For a savings plan (endowment or money-back), a longer term means more years of guaranteed savings build-up, so the yearly premium is higher, but so is the maturity payout.

- Plan type. This is the biggest lever of all. A pure term plan can cost a small fraction of an endowment plan for the identical sum assured, because you are buying protection only, not protection plus savings. If the gap surprises you, read term vs endowment in Nepal before deciding which you actually want.

One thing that does not change your premium much: which insurer you pick. Across Nepal’s licensed life insurers, base rates for a given plan type sit close together, so the same profile produces broadly similar premiums everywhere. The real differences show up in claim-settlement records, bonus rates, and financial strength, not the headline price. Compare on those, not on a few hundred rupees of premium.

Payment term is not the same as policy term

This trips up more buyers than any other premium fact. The policy term is how long your cover lasts. The premium-payment term is how long you actually keep paying. On many Nepali plans they are the same: a 20-year policy where you pay for all 20 years. But “limited-pay” plans deliberately separate them, so you might finish paying a few years before the cover ends, or pay for the bulk of the term and ride out the last stretch fully paid.

Why it matters: when you read a quote, check how many years of premiums you are committing to, not just how long the cover runs. A plan that looks affordable per year can demand payments for nearly the entire term, and the lapse rules below make every one of those payments matter.

Grace periods, lapse, and revival: keeping the policy alive

A premium you forget to pay is the fastest way to lose everything you have built. Here is how the safety net works:

- Grace period (usually 30 days). Miss a due date and you still have a grace window, typically around 30 days, to pay without penalty and keep the policy fully in force.

- Lapse. Let the grace period pass and the policy lapses: you lose the life cover, your riders (such as Accidental Death Benefit), and access to accrued bonuses. A claim during a lapse can be denied outright.

- Revival. A lapsed policy can often be revived. You contact your branch, clear the unpaid premiums (sometimes with interest), and may need to re-confirm your health. But the revival window does not stay open forever, so act fast.

Missing payments is one of the most common and most avoidable policyholder mistakes; we cover the full list in 5 life insurance mistakes Nepalese policyholders make. The practical fix is dull but decisive: set a reminder and automate the payment through eSewa, Khalti, or ConnectIPS.

The number that shocks endowment buyers: total premiums vs sum assured

Here is the arithmetic almost no agent walks you through. Take a typical 20-year endowment plan for a sum assured of NPR 10 lakh, bought around age 30 to 35. In our calculator’s model that runs roughly NPR 49,000 to 53,000 per year. Over the full 20 years, that is about NPR 9.8 to 10.7 lakh in premiums: essentially the entire base sum assured, and at the upper end, more than it.

Not sure which plan fits you? Answer 5 questions and get a personalised match.

Find My Plan →That is not a scam; it is how endowment is built. You are not “losing” money. The plan only makes sense because bonuses accumulate on top of the sum assured, and the maturity payout is the sum assured plus those bonuses. But it reframes the decision: an endowment premium is mostly forced savings with a life-cover wrapper, not a cheap way to buy protection. If your priority is the largest possible cover for the lowest outlay, a term plan delivers the same NPR 10 lakh of protection for a small fraction of that yearly cost. The trade-off (protection-only vs protection-plus-savings) is the whole of term vs endowment.

Can you reduce a premium after the policy is issued?

Partly. You generally cannot just lower the agreed premium on the same policy on a whim, because the premium is tied to the sum assured and term you locked in. But if the payments have become genuinely unaffordable, you have options short of walking away and losing money:

- Paid-up conversion. If you have paid premiums for the minimum qualifying period, you can stop paying and convert to a “paid-up” policy with a reduced sum assured. The cover shrinks, but it survives and still pays out at maturity.

- Reduce the cover going forward where the plan allows it, lowering future premiums.

- Use the policy’s own value to bridge a tight period rather than surrendering, because surrender is almost always the worst-value exit – see how a policy loan in Nepal works.

Talk to your branch before you stop paying. Once a policy lapses without using one of these routes, you are back to the revival rules above.

Quick answers

Does my premium increase every year?

No. On a standard endowment or term plan the premium is level, fixed for the life of the policy at the rate set when you bought it. That is exactly why buying younger is cheaper: you lock the lower rate in permanently.

Is it cheaper to pay yearly or monthly?

Yearly is almost always the cheapest mode. Splitting into half-yearly, quarterly, or monthly instalments usually adds a small loading, so you pay a little more over the year for the convenience.

What happens to the premiums I’ve already paid if I stop?

It depends on how far in you are. Early on, a lapse can mean losing the lot. After the qualifying period, you can convert to a paid-up policy and keep a reduced benefit. Never just stop paying without asking your branch which applies to you.

Price it for yourself

The fastest way to understand your own premium is to move the sliders and watch the number change. Try a few ages, terms, and sums assured in our free premium calculator (no sign-up, no agent call), then compare the insurers on what actually matters: claim settlement, bonuses, and financial strength.

Independent and free. We don’t sell policies. We help you understand them.