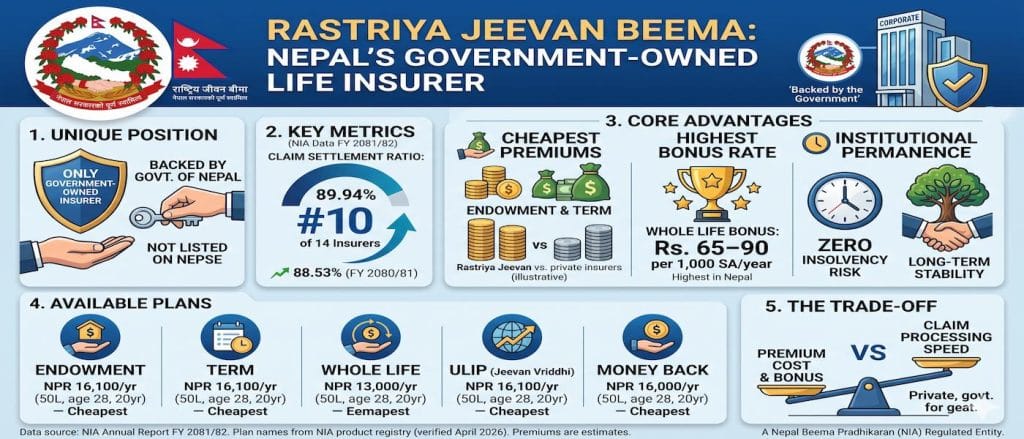

Rastriya Jeevan Beema holds a unique position in Nepal’s market: it is the country’s first life insurer and the only government-owned one, established by the Government of Nepal (and restructured from the former Rastriya Beema Sansthan into Rastriya Jeevan Beema Company Limited in late 2023). On our derived measure it sits at 89.94% for FY 2081/82, ranking #10 of 14 and improving year on year. Its endowment and term base rates are the lowest in our data. This review covers its plans, how reliably it pays, and who it suits.

Quick Facts

| Detail | Information |

|---|---|

| Full name | Rastriya Jeevan Beema Company Limited |

| Ownership | Government of Nepal (only government-owned life insurer) |

| Regulator | Nepal Beema Pradhikaran (NIA) |

| Market share (premium) | 5.43% |

| Life fund | NPR 62.30 arba (one of the largest) |

| Claim ratio FY 2081/82 (derived) | 89.94% (rank #10 of 14) |

| Claim ratio FY 2080/81 (derived) | 88.53% (improving) |

| Total claims paid FY 2081/82 | NPR 6.56 billion (Rs. 656.19 crore) |

| Entry age | 16 – 60 years (adult plans) |

| Policy terms | 5 – 25 years |

| Riders | Accident, Disability |

Claim Settlement Ratio: #10, and Improving

An honest note on the number first. The NIA does not publish a per-company “claim settlement ratio.” It publishes claims paid and claims outstanding for each insurer, and the 89.94% here is a ratio we derive from those (claims paid divided by claims paid plus outstanding). It is amount-based, a year-end snapshot, and excludes rejected claims.

Rastriya Jeevan Beema ranks #10 of 14, and the direction is positive: it rose from 88.53% to 89.94% year on year. In FY 2081/82 it paid Rs. 656.19 crore (about NPR 6.56 billion) in claims, with roughly a tenth of its claim value still outstanding at year-end – a larger pending share than the market’s top payers, which is what holds the percentage below the leaders. Read it for what it is: an amount-based snapshot of a pending queue, not a count of denied claims, so it is fair to ask the company about its settlement timelines rather than to read it as outright refusal.

Plans Available (FY 2081/82)

Endowment: Jeevan Surakshya (flagship)

Its main savings-plus-protection plan, and one of a broad endowment menu it sells (others include Jeevan Bandhu, Endowment Life Assurance, the Joint Life “Jeevan Sathi” plan, and the Bal Umanga child plan). It pays the sum assured plus accumulated bonus at maturity, or the full sum assured to your nominee on death during the term. See the full list on Rastriya Jeevan Beema’s own site.

- Endowment bonus (FY 2081/82): not declared at the time the other 13 insurers declared theirs – confirm the current rate with the company

- Riders available: Accident, Disability

- Policy loan: Yes, after 3 years | Surrender: Yes

Term: Term Life Assurance (flagship)

Pure life protection – the highest cover for the lowest premium. Rastriya Jeevan Beema’s term base rate is the lowest in our data, so it is well worth a look if price is your priority.

Whole Life and Anticipated (Money Back)

It offers whole-life cover and an Anticipated Endowment Life Assurance plan (a money-back style plan that returns cash during the term while keeping life cover in force). It also runs government-oriented schemes such as Rastra Sewak Insurance for public servants, a Foreign Employment plan, and micro-insurance.

The Government-Ownership Factor

The genuine draw of Rastriya Jeevan Beema is what it is: the country’s first life insurer, owned by the Government of Nepal, with one of the largest life funds in the market (NPR 62.30 arba). That gives it a sense of institutional permanence many buyers value.

Don't buy based on reviews alone. Compare claim ratios and IRR instantly.

Compare All PlansIt is worth being precise about what that does and does not mean. Government ownership signals longevity and reduces the perceived risk of the company disappearing. It is not, however, a formal legal guarantee that individual policy payouts are state-backed – Nepal has no separate sovereign guarantee scheme for life policies, and every insurer here, government or private, operates under the same NIA solvency rules and the same regulator. So treat the government tie as reassurance about institutional stability, not as a promise of zero risk.

A Note on Bonus Rates

Here is the one genuinely unusual thing about its bonus. For FY 2081/82, 13 of Nepal’s 14 life insurers declared endowment bonus rates; Rastriya Jeevan Beema was the exception that had not. It has paid bonuses historically, but as a government insurer its declaration schedule is less predictable than the privates’. For that reason we do not publish a current bonus figure for it. If bonus accumulation is central to your decision, ask the company directly for its latest declared rate before you buy, and compare it against our comparison of all 14 companies.

Who Should Choose Rastriya Jeevan Beema?

Choose Rastriya Jeevan Beema if:

- Price is your top priority – its endowment and term base rates are the lowest in our data

- You value a long-established, government-owned institution with one of the largest life funds in the market

- You are a public servant or going for foreign employment and want a scheme built for that

Consider alternatives if:

- The claim record is your main criterion – Asian Life (98.85%), Sun Nepal (98.71%), and several others rank well above on this measure

- A predictable, published bonus matters to you – the other 13 insurers declared FY 2081/82 rates and this one had not

- You need entry below age 16, a term beyond 25 years, or a Critical Illness rider

See Your Own Numbers

Premiums depend on your age, sum assured, and term, so a single sample figure can mislead. Use the Premium Calculator to compare Rastriya Jeevan Beema’s estimated premium against all 13 other insurers for your exact inputs.

Data source: NIA Annual Report FY 2081/82 (Schedules 14 and 15) for financials and claim amounts; plan names from Rastriya Jeevan Beema’s own website. The claim “ratio” is our amount-based derivation (claims paid over paid plus outstanding, in NPR crore); the NIA does not publish a per-company settlement ratio. Any premium shown by our calculator is an estimate, not a quote. Full disclaimer.