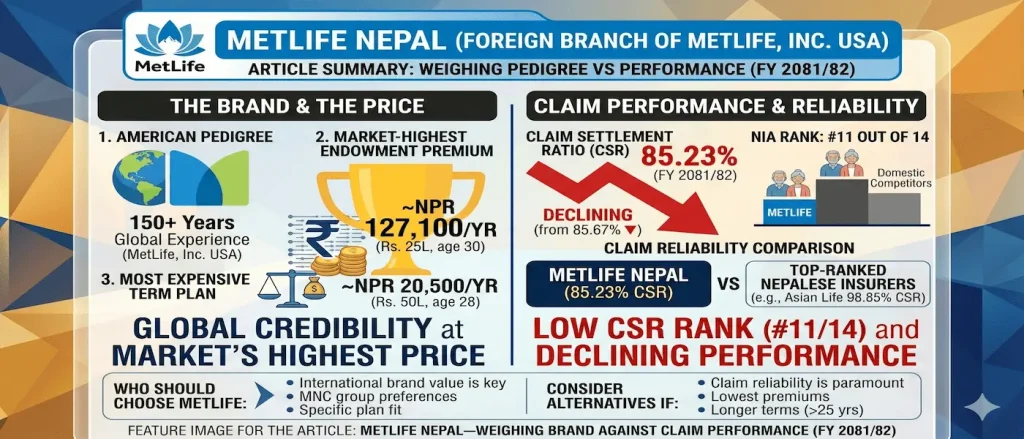

MetLife Nepal is the country’s only American multinational life insurer – the local branch of MetLife, Inc., which has insured lives for more than 150 years across some 40 countries. It entered Nepal in 2001 as the first foreign insurer in the market. That global parentage shapes what MetLife is here: less a sprawling retail menu of traditional Nepali policies, and more a focused mix of savings, education, health, and employer/group cover backed by an international balance sheet.

Quick Facts

| Detail | Information |

|---|---|

| Full name | MetLife (American Life Insurance Company, Nepal Branch) |

| NEPSE symbol | N/A (foreign branch, not listed) |

| Established in Nepal | 2058 BS (2001 AD) – first foreign insurer in Nepal |

| Type | Foreign branch |

| Parent company | MetLife, Inc. (USA) |

| Market share (premium) | 3.45% |

| Life fund | NPR 29.58 arba |

| Claim ratio FY 2081/82 (derived) | 85.23% (rank #11 of 14) |

| Claim ratio FY 2080/81 (derived) | 85.67% (declining) |

| Total claims paid FY 2081/82 | NPR 2.95 billion (Rs. 294.62 crore) |

| Individual entry age | 18 – 60 years (Midterm Growth) |

Claim Settlement Ratio: #11, and What That Number Means

An honest note on the figure first. The Nepal Insurance Authority (NIA) does not publish a per-company “claim settlement ratio.” It publishes two separate amounts per insurer: claims paid and claims outstanding. The 85.23% you see here is a ratio we derive from those NIA amounts (claims paid divided by claims paid plus outstanding). It is amount-based and excludes rejected claims – it is not a count of “85 out of every 100 claims paid.”

On that measure MetLife Nepal sits at 85.23% for FY 2081/82, ranking #11 of Nepal’s 14 life insurers, slightly below its 85.67% the previous year. In rupee terms it paid Rs. 294.62 crore (about NPR 2.95 billion), down from Rs. 323.54 crore a year earlier, against Rs. 51.06 crore still outstanding at year-end.

One thing worth understanding about a smaller-volume insurer like MetLife: an amount-based ratio is sensitive to a handful of large claims sitting in the outstanding column at the close of the year, so it can move year to year more than a giant insurer’s would. Read this number alongside MetLife’s global backing and its service record, rather than as the whole story on its own.

What MetLife Nepal Actually Sells

Unlike most Nepali insurers, MetLife does not offer an individual whole-life plan, and its retail line-up leans toward savings, term protection, and health rather than the full endowment-term-whole-life-money-back menu. Its real depth is in health and group/employer cover. Here is what it offers.

Midterm Growth Plan (anticipated endowment)

MetLife’s flagship individual savings plan, and the most interesting in its structure. It pays out in two phases and boosts the death cover partway through:

- Survival payouts: 40% of the face amount at the policy midterm, then 60% plus accrued bonuses at maturity

- Death benefit: 100% of face amount plus bonuses before midterm; 200% plus bonuses after midterm (the 40% midterm payout is not deducted)

- Terms and entry: policy terms of 12 to 22 years; entry age 18 to 60; face amount Rs. 250,000 to Rs. 50,000,000

- BonusExtra money declared annually by the insurer on top of your sum assured. Full definition →: participates in profits via reversionary bonuses (MetLife does not publish a fixed rate for this plan)

- Riders: Personal Accident, Waiver of PremiumThe regular payment you make to keep your insurance policy active. Full definition →, Critical Illness; policy loan and surrender options available

Subhabisya Beema (retirement income)

A long-term savings plan aimed at building guaranteed income for after retirement, rather than a classic endowment. (Note: our calculator currently models Subhabisya as MetLife’s endowment-type plan for comparison purposes.)

LifeCare (term life)

MetLife’s individual term plan, which sits under its Life and Health range. LifeCare pays a lump sum on loss of life, with optional add-ons for critical illness, and comes in three packages: LifeCare – My Life (pure loss-of-life cover at the lowest premium), LifeCare – Beautiful (loss of life plus a female critical-illness benefit covering nine conditions), and LifeCare – Brave (loss of life plus a general critical-illness benefit covering fourteen conditions).

Don't buy based on reviews alone. Compare claim ratios and IRR instantly.

Compare All Plans- Entry age: 18 to 60

- Policy terms: 1, 5, 10, 15, or 20 years

- Sum assured: NPR 200,000 up to NPR 15,000,000 on the My Life (loss-of-life) package

- UnderwritingThe process by which an insurer evaluates your health and risk before issuing a policy. Full definition →: no medical check-up within MetLife’s non-medical limits

If pure, low-cost life cover is what you want, LifeCare – My Life is MetLife’s offering for it; the Beautiful and Brave packages bundle in critical-illness protection for a higher premium.

Other plans

- Future Care DPS and Double Protection Plus – savings and investment plans

- My Child’s Education Protection Plan – education savings for a child’s future

- Life Shield – health and accident cover

- Group Life, Group Affinity, and Micro Insurance – employer and group cover, where MetLife’s multinational experience is strongest

For completeness: MetLife Nepal does not offer an individual whole-life plan. Its individual range is endowment-style savings (Midterm Growth, Subhabisya), term life (LifeCare), and a child education plan, alongside its health and group cover.

Bonus note: MetLife’s company-level declared endowment bonus for FY 2081/82 is Rs. 50 to Rs. 70 per 1,000 sum assured (reported by Beemapost and Insurance Khabar). The reversionary bonus rate on Midterm Growth specifically is not publicly disclosed – confirm the declared rate for your exact plan and term before buying.

Who Should Choose MetLife Nepal?

MetLife is a strong fit if:

- You value a globally backed, multinational insurer and the financial strength of MetLife, Inc.

- Your employer offers MetLife group or affinity benefits – this is where its international experience runs deepest

- The Midterm Growth structure appeals to you – liquidity partway through the term plus doubled death cover in the later phase

- You want savings, education, and health cover from a single international brand

Worth knowing before you decide:

- MetLife has no individual whole-life plan, so if that is specifically what you want, you will need to look at another insurer

- Its derived claim ratio (85.23%, #11 of 14) currently trails Nepal’s top-ranked insurers – a point to weigh alongside the global brand and the specific plan you are considering

Use the Compare Plans tool to see MetLife Nepal alongside the other 13 insurers for your exact age, sum assured, and term. Not sure which plan suits you? Try Find Your Life Insurance Plan.

Data source: NIA Annual Report FY 2081/82 for financials and claim amounts; product details from MetLife Nepal’s own website (metlife.com.np); bonus rates from Beemapost and Insurance Khabar. The claim “ratio” is our amount-based derivation (claims paid over paid plus outstanding, in NPR crore per NIA Schedules 14 and 15); NIA does not publish a per-company settlement ratio. Any premium shown by our calculator is an estimate, not a quote. Full disclaimer.