If your family relies on the income you earn abroad, their financial stability is tied to your well-being. You can use Nepal’s evolving life insurance market to make sure they are taken care of, no matter what happens.

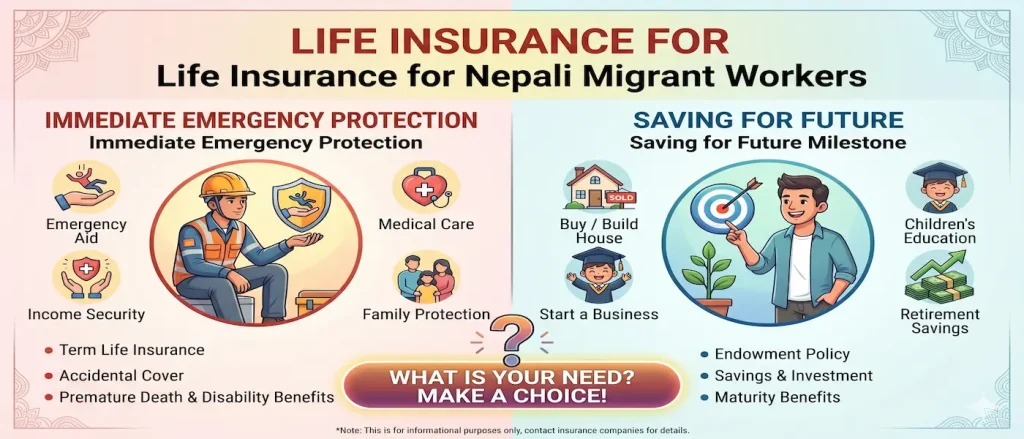

- To cover major debts or future costs (High-Leverage Protection): You can buy a Term Life Insurance Policy (such as SuryaJyoti’s Suraksha Kawaj or MetLife’s Term plans). These don’t build savings, but they are very affordable and pay out a large lump sum. If you took out a mortgage to build a family home in Nepal, this prevents creditors from forcing your family to sell the house if you are no longer there.

- To save for milestones (Blended Security): You can look into Endowment or Anticipated (Money-Back) Plans (from providers like Nepal Life or Sunlife). These act as forced savings. If you plan to return to Nepal in 10 years to start a business, or if your children will hit college age, these policies pay out guaranteed lump sums at specific intervals or upon maturity.

- To leave a lasting legacy (Wealth Transfer): A Whole Life Insurance Policy ensures that your children or spouse inherit an unencumbered financial legacy, providing them with immediate cash to handle property inheritance costs or long-term living expenses.

2. Secure Your Baseline Mandatory Coverage (For Migrant Workers)

If you are traveling on a temporary labor permit (Shram Swikriti), the government mandates a Foreign Employment Term Life Insurance policy. It is highly subsidized and acts as your primary shield against harsh overseas work environments.

What This Covers for Your Family:

The premium is low (roughly NPR 3,308 to NPR 9,063 for a 2-year contract depending on your age), but the protective return for your family is substantial:

| What It Protects | How Much It Pays to Your Family / Nominee |

| Basic Death Coverage | NPR 1,000,000 lump sum if the worst happens. |

| Critical Illness | NPR 500,000 accelerated payout to fund immediate medical care. |

| Disability | 5% to 100% of basic coverage depending on injury severity. |

| Loss of Income / Repatriation | NPR 200,000 bridging support if you are forced to return home due to injury/illness. |

| Funeral & Body Repatriation | NPR 100,000 each to lift the immense logistical and ceremonial financial burdens from your family during a crisis. |

3. Manage Everything Remotely Without Flying Back to Kathmandu

You do not need to spend money on plane tickets or take time off work to set up or maintain these safety nets. The industry has gone digital to accommodate the diaspora.

- Get Verified via Video KYC: You can buy a policy entirely from abroad. Using portals like Citizen Life or MetLife, you upload your documents (like your Passport or NRN ID card) and complete a Video KYC (Know Your Customer) call via encrypted channels like WhatsApp. Advanced systems verify your location and identity securely from your phone.

- Pay Premiums Instantly: You can prevent your policy from lapsing by paying premiums through eSewa, Khalti, IME Pay, or ConnectIPS. If you have an active bank account in Nepal, you can use mobile banking apps powered by Fonepay to pay instantly via dynamic QR codes.

- Handling Large Amounts: If you are managing a high-value policy where the premium exceeds digital wallet limits (NPR 200,000), you can use a SWIFT wire transfer directly from your foreign bank to the insurer’s Nostro/Vostro accounts in Nepal (e.g., via Nepal Investment Mega Bank).

4. Maximize Tax Savings on Your Assets in Nepal

If you still earn an income within Nepal (like rental income, business revenue, or investments), you can use your life insurance to shield that money from heavy taxation.

- The Inland Revenue Department allows you to deduct up to NPR 40,000 per year from your taxable income for life insurance premiums paid.

- If you and your spouse file taxes together in Nepal, you can club your payments to maximize this deduction, keeping more cash in your family’s pockets.

5. Prepare Your Family for Cross-Border Claims

If your family ever needs to claim a payout while you are residing or working abroad, the process requires strict documentation to avoid delays. You should educate your designated nominee (your spouse, child, or parent) on these steps:

- The Death Certificate: If a mortality event happens abroad, the local death certificate must be authenticated by the nearest Nepalese Embassy or Consulate in that foreign country before a domestic insurer will accept it.

- Required Documents: Your family will need the original policy document (Daabi Farchhaut Purja), their own Nepali Citizenship certificate, proof of relation, and medical/police reports if it was an accident.

- Use Digital Portals: Companies like Sunlife and Nepal Life now have online claim-request portals so your family can start the process immediately while waiting for physical paperwork to clear consular channels.

If you are not sure which plan is best for you, check which Life Insurance Plan is best for you.