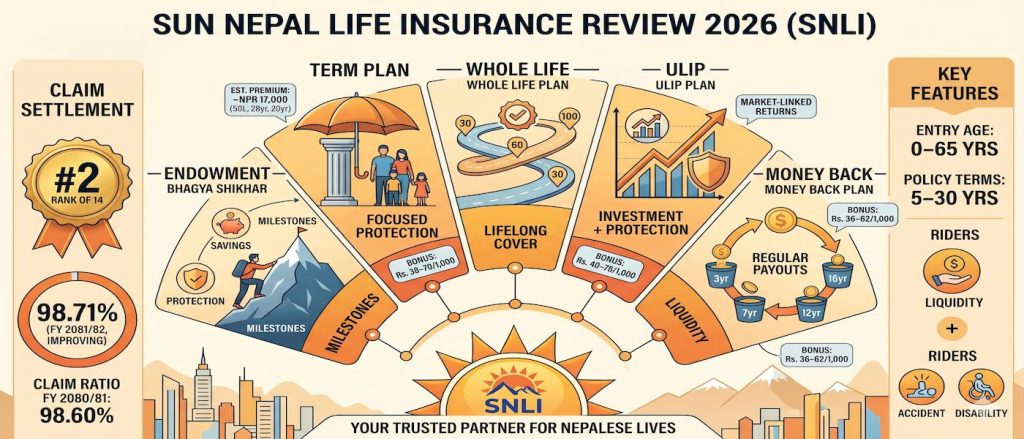

Sun Nepal Life Insurance holds the second-highest claim settlement ratio of Nepal’s 14 life insurers on our derived measure – 98.71% for FY 2081/82, improving from 98.60% the year before, and backed by a very clean claims pipeline. If paying claims reliably is your first priority, Sun Nepal sits right at the top alongside Asian Life.

Quick Facts

| Detail | Information |

|---|---|

| Full name | Sun Nepal Life Insurance Company Limited |

| NEPSE symbol | SNLI |

| Type | Private, Nepali-owned |

| Regulator | Nepal Beema Pradhikaran (NIA) |

| Market share (premium) | 2.76% |

| Life fund | NPR 10.10 arba |

| Claim ratio FY 2081/82 (derived) | 98.71% (rank #2 of 14) |

| Claim ratio FY 2080/81 (derived) | 98.60% (improving) |

| Total claims paid FY 2081/82 | NPR 1.57 billion (Rs. 157.34 crore) |

| Entry age | 18 – 65 years (adult plans) |

| Policy terms | 5 – 30 years |

Claim Settlement Ratio: A Clean #2

An honest note on the number first. The NIA does not publish a per-company “claim settlement ratio.” It publishes claims paid and claims outstanding for each insurer, and the 98.71% here is a ratio we derive from those (claims paid divided by claims paid plus outstanding). It is amount-based and excludes rejected claims.

Sun Nepal’s record is genuinely strong. In FY 2081/82 it paid Rs. 157.34 crore (about NPR 1.57 billion) in claims against only about Rs. 2 crore outstanding at year-end – one of the cleanest paid-to-outstanding balances in the market, and improving year on year. That puts it second only to Asian Life on our measure. As always, an amount-based ratio cannot show settlement speed, so it is still fair to ask about timelines.

Plans Available (FY 2081/82)

Endowment: SunLife Endowment Assurance (flagship)

Sun Nepal’s main savings-plus-protection plan, and one of several endowment plans it sells (others include the single-premium Bhagyodaya and the Sun Life Endowment Golden plan). It pays the sum assured plus accumulated bonus at maturity, or the full sum assured to your nominee on death during the term. See the full list on Sun Nepal’s own site.

- Endowment bonus (FY 2081/82): Rs. 33 to Rs. 70 per 1,000 sum assured per year

- Riders available: Accident, Disability

- Policy loan: Yes, after 3 years | Surrender: Yes

Term: Nabikaran Myadi (flagship)

A renewable term plan – cost-effective pure life protection for a chosen period, with the option to renew.

Whole Life: Saarthak Ajeewan (flagship)

A lifetime plan that provides long-term cover with periodic returns, suited to buyers who want lasting protection and a legacy for the next generation.

Don't buy based on reviews alone. Compare claim ratios and IRR instantly.

Compare All PlansMoney Back: Dhananjaya (flagship)

An anticipated-endowment / money-back plan (Dhananjaya Yearly Moneyback Endowment) that returns part of the sum assured each year during the term, with life cover throughout – useful for predictable expenses like education or celebrations.

A Note on Bonus Rates

Sun Nepal’s declared endowment bonus for FY 2081/82 is Rs. 33 to Rs. 70 per 1,000 sum assured (dual-sourced from Beemapost and Insurance Khabar) – a mid-market range, so its appeal is claim reliability rather than peak bonus. Its other plans carry their own declared rates, so confirm the bonus for the specific plan and term you are buying. To weigh insurers side by side, see our comparison of all 14 companies.

Who Should Choose Sun Nepal Life?

Choose Sun Nepal Life if:

- You put claim reliability first – it ranks #2 on our derived measure (98.71%), improving, with a very clean paid-to-outstanding balance

- You need entry up to age 65 or a 30-year policy term

- You prefer a fully Nepali-owned insurer with a steady top-of-market record

Consider alternatives if:

- You want the highest possible bonus – National Life (up to Rs. 85) and Nepal Life (up to Rs. 82) declare higher endowment ranges than Sun Nepal’s Rs. 33 to Rs. 70

- You specifically need a Critical Illness rider – confirm availability with Sun Nepal, as it is not listed among its standard riders

See Your Own Numbers

Premiums depend on your age, sum assured, and term, so a single sample figure can mislead. Use the Premium Calculator to compare Sun Nepal Life’s estimated premium against all 13 other insurers for your exact inputs.

Data source: NIA Annual Report FY 2081/82 (Schedules 14 and 15) for financials and claim amounts; plan names from Sun Nepal Life’s own website; bonus rates from Beemapost and Insurance Khabar. The claim “ratio” is our amount-based derivation (claims paid over paid plus outstanding, in NPR crore); the NIA does not publish a per-company settlement ratio. Any premium shown by our calculator is an estimate, not a quote. Full disclaimer.