What is Term Insurance in Nepal? The Complete Beginner’s Guide

If you have ever asked an insurance agent “what is the cheapest way to protect my family?” — term insurance is the honest answer. Yet it is also the product agents are least likely to recommend, because it pays them the lowest commission.

This guide explains exactly what term insurance is, how it works in Nepal, who should buy it, and what it costs from each of Nepal’s 14 NIA-licensed life insurers.

The Simple Definition

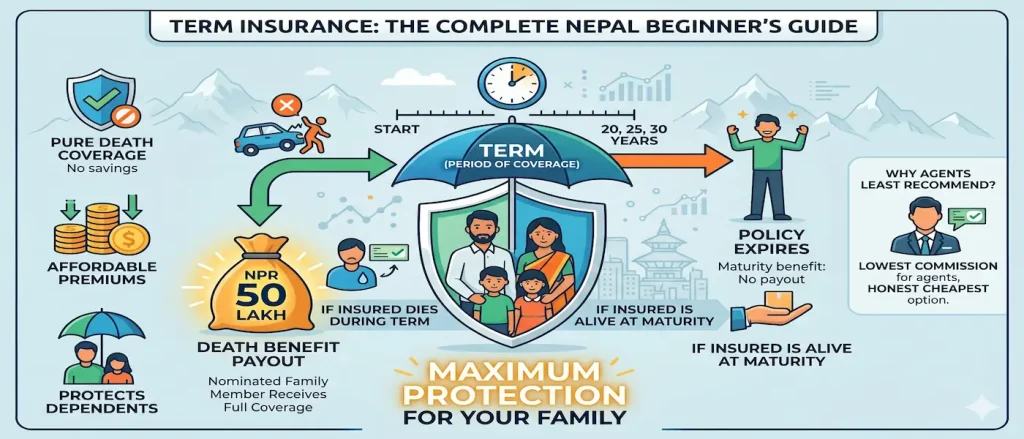

Term insurance is a type of life insurance that provides pure death coverage for a fixed period — the “term.” If you die during this period, your nominated family member receives the full coverage amount (sum assured). If you are still alive when the term ends, the policy expires and you receive nothing back.

That last part — receiving nothing at maturity — is what most people find uncomfortable. But it is also exactly why term insurance is so affordable. The insurance company is only covering the risk of your death. There is no savings component, no investment, no maturity payout to fund. The premium is purely the cost of protection.

How Term Insurance Works — A Real Nepal Example

Bikash is 32 years old, married with two young children, and works as a civil engineer in Kathmandu earning NPR 80,000 per month. He buys a pure term plan from one of Nepal’s licensed insurers:

Not sure which plan fits you? Answer 5 questions and get a personalised match.

Find My Plan →- Sum assured: NPR 50 lakh

- Policy term: 25 years (until he is 57)

- Annual premium: in our calculator’s model, around NPR 20,000 a year (it varies by insurer)

Scenario A — Bikash dies at age 44 in an accident. His wife receives NPR 50 lakh as a tax-free lump sum. This replaces roughly 5 years of his income — enough time for his family to adjust, pay off loans, and get the children through school.

Scenario B — Bikash reaches 57 with the policy intact. The policy expires. Bikash receives nothing. But for 25 years, his family was protected for around NPR 20,000 a year — under NPR 2,000 per month.

Term Insurance vs Endowment — The Key Difference

| Feature | Pure Term Plan | Endowment Plan |

|---|---|---|

| Annual premium | Lowest (protection only) | Much higher (protection + savings) |

| Death benefit | NPR 50 lakh | NPR 50 lakh + bonus |

| Maturity benefit | Nothing | NPR 50 lakh + bonus |

| Loan facility | No | Yes (after 3 years) |

| Tax deduction on premium | Yes | Yes |

| Best for | Maximum protection, tight budget | Forced savings, specific goal |

Who Should Buy Term Insurance?

Young earners with dependents. If you have a spouse, children, or parents who depend on your income, term insurance gives you the maximum coverage for the lowest possible cost.

People with home loans or large debts. A term plan sized to cover your outstanding loan balance ensures your family keeps the house if you die.

Remittance workers abroad. If you are working in the Gulf, Malaysia, or elsewhere, all 14 Nepal life insurers cover death outside Nepal as standard.